How Net Unrealized (NUA) Tax Strategies Can Lower Your Taxes in Retirement

Normally, transferring qualified retirement funds into an individual, joint or trust account triggers ordinary income tax on the total amount that was transferred. But, when it comes to transferring employer stock, the IRS allows special tax treatment called Net Unrealized Appreciation, or “NUA” for short.

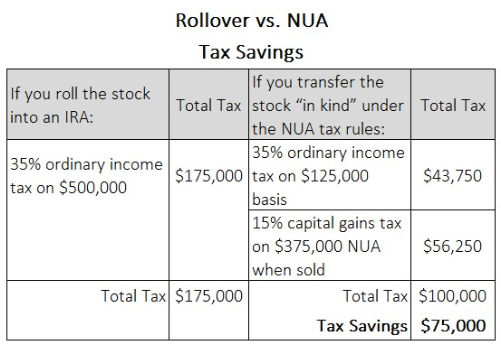

The amount you paid for the stock, also known as “cost basis,” is taxed at your ordinary income tax rates in the year of distribution. The difference between your cost basis and the current market value of the stock is taxed at the long-term capital gains rate in effect at the time the stock is sold. If the stock continues to appreciate before you sell, you will pay long or short-term capital gains rates depending on the holding period. The higher your income tax bracket and the more the stock has appreciated, the bigger the tax benefit you will receive.

An Example:

Let’s assume the following:

- your 401(k) contains $500,000 worth of Coca-Cola stock

- you purchased your shares with pre-tax contributions for $125,000 (your cost basis)

- your Net Unrealized Appreciation is $375,000

- you’re in the 35% tax bracket

If you do not sell the stock right away, any additional appreciation above the $500,000 is taxed as a short-term or long-term gain, depending on how long you hold the stock after distribution. If the value of the shares falls below $500,000, any depreciation can be claimed as a short or long-term loss.

Other Things You Need to Know Before You Elect NUA

- Contact your former employer to make sure your employer plan allows for “in-kind” distributions of company stock.

- You must experience one of these triggering events: terminate employment, be at least age 59 ½, become totally disabled, or die.

- A 10% early withdrawal penalty on the cost basis applies to those who are under age 59 ½, potentially negating all or some of the tax benefit.

- You will need to confirm with your employer that the shares of stock were purchased with pretax contributions and/or employer matches.

- Your entire vested balance in the plan must be distributed in a lump sum within one tax year. That means you should not take distributions from the employer plan in years before the year you want to do the NUA, or else your distribution of the stock in a subsequent year will not qualify as a lump sum distribution.

- You must distribute all assets from all qualified plans at your former employer, not just the one that held the shares of stock.

- Assets outside a qualified employer plan or individual retirement account (IRA) may have less protection from creditors’ claims.

- If the stock price declines or tax rates change, this could defeat the tax-saving benefits of the NUA strategy.

- Deciding whether NUA makes sense for your situation depends on a number of factors. If by rolling to an IRA taxes can be deferred for a long time and/or paid at lower rates, a lump sum may not be desirable.

- NUA does not enjoy a “stepped-up basis” at death. However, any additional appreciation between the date of distribution and the date of your death would not be subject to income tax because, under current law, the beneficiaries would be entitled to obtain a “stepped up” basis in the shares they inherit.

- Tax laws can and do change, so it’s important to make sure you understand the laws before you make your decision.

- Incurring additional income via NUA could unintentionally and negatively impact your overall financial picture. For example, the monthly premiums you pay for Medicare services could go up, more of your Social Security benefit could be subject to tax, and some of your allowable itemized deductions may be reduced, just to name a few. It is important to consult a tax advisor to discuss your specific circumstances and how NUA may affect your overall tax bill.

Net Unrealized Appreciation (NUA) and Your Required Minimum Distribution (RMD)

Keep in mind that both the cost basis and the NUA portion count toward your RMD after age 70 ½, so there should be no need to hold back any other assets for your RMD as long as the total market value of the shares distributed is enough to meet your RMD requirement. Because the shares are distributed “in kind,” no taxes are withheld at the time of distribution or subsequent sale. In order to avoid any tax underpayment penalties, you will need to make sure you have paid enough tax in advance through withholding and/or quarterly estimated tax payments. If it looks like you will be substantially short, you can increase withholding from income sources that withhold tax payments or make a quarterly estimated tax payment to Uncle Sam to cover the difference.

If you’re expecting a distribution of employer securities from a qualified retirement plan, make sure you speak with a financial advisor and tax preparer before you take any action to make certain understand all the options available to you. Only then can you be assured of making the decision that best meets your individual financial goals.